How to Write Release Notes When the Regulators Are Reading

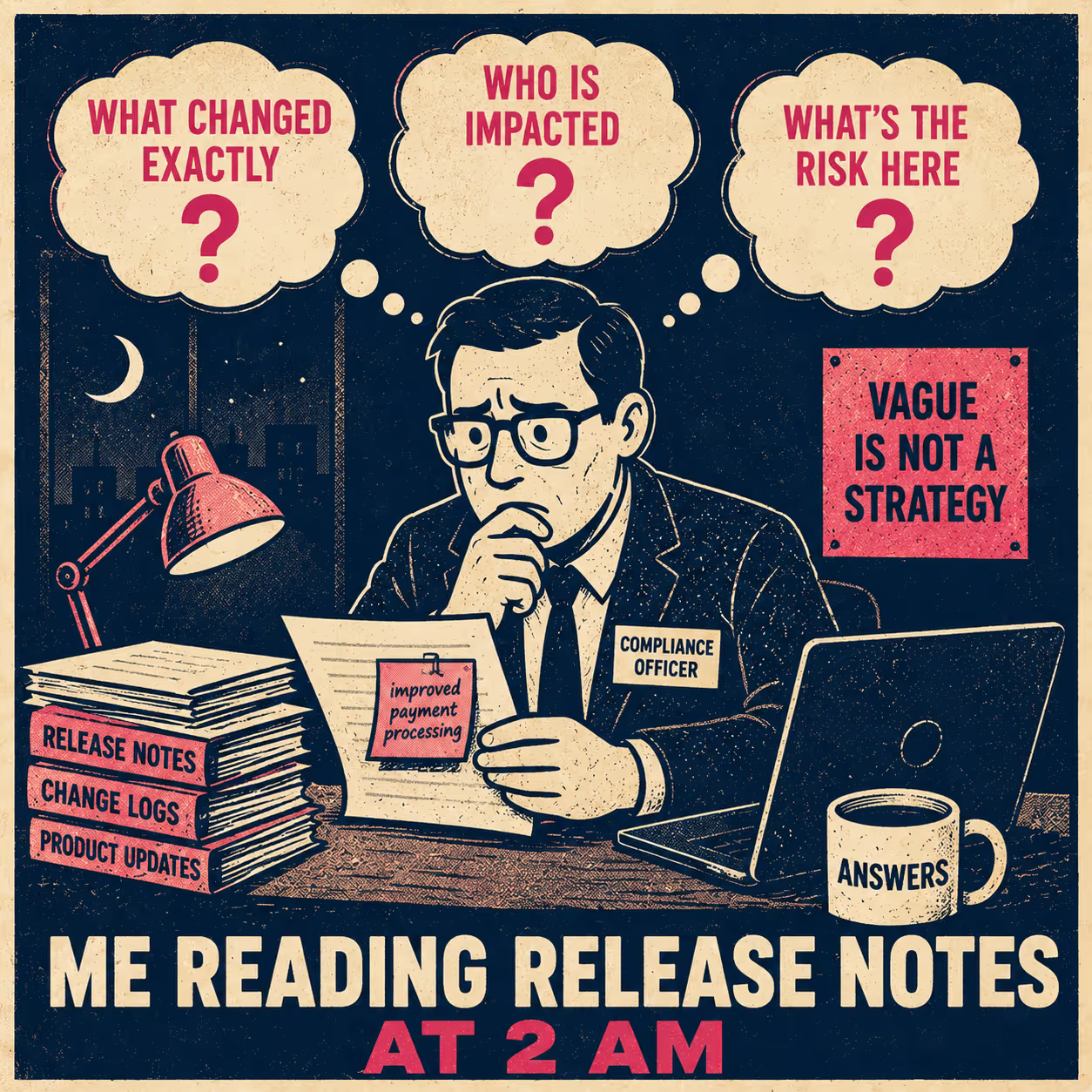

A compliance officer at a mid-sized payments company gets a release note. It says "improved payment processing." That's it.

She doesn't know if this is a routing change. She doesn't know if it affects the settlement batch that runs at 2 a.m. She doesn't know if her reconciliation job will break. So she files a support ticket. The support team escalates to engineering. Engineering says it was a minor optimization to the retry logic. No impact on settlement. But by then, three days have passed, and the auditor is asking for documentation of the change that went out last month.

The note said "improved payment processing." The auditor wants to know who authorized it, what was tested, and what the rollback plan was.

This is the specific problem with fintech release notes. They serve two audiences with almost no overlap. Auditors want evidence. Users want reassurance. And both of them are reading the same document.

What Auditors Actually Want to See

SOC 2 Common Criteria 8.1 requires organizations to authorize, design, develop, test, approve, and implement changes to data, software, or processes (AICPA, 2017). Auditors will sample a set of changes from the audit period and look for corresponding documentation. If a change was deployed but not documented, or if the documentation doesn't match the deployed change, that's a finding.

PCI-DSS 6.5 has similar requirements for change control, including documentation of impact, testing procedures, and back-out procedures for changes to in-scope systems (PCI Security Standards Council, 2022). The FFIEC's Development, Acquisition, and Maintenance booklet, updated in August 2024, directs examiners to assess whether financial institutions follow established change management policies, standards, and procedures to plan, test, and document changes before implementation (FFIEC, 2024).

What this means in practice: your release notes need to contain, at minimum, a change identifier (ticket number or commit hash), a description of what changed and why, a record of who approved it, and a note on what was tested. That's the compliance floor. Everything else is operational preference.

The distinction matters. Compliance teams at fintech companies sometimes over-engineer their release notes, adding legal review cycles that slow down deployment. But the regulatory frameworks don't require prose. They require traceability. A structured entry with a ticket reference, a change type, and an approval timestamp satisfies an auditor. A paragraph of marketing copy does not.

Compliance-forward fintechs tend to separate the two layers explicitly. The internal change record, which lives in the issue tracker and contains the technical detail, is the audit artifact. The external release note, which is user-facing, is derived from it. The two are linked by a ticket reference. When the auditor asks for documentation of a change, you pull the ticket. When the user asks what changed, you point to the release note. Neither document tries to do both jobs.

The User Communication Problem Nobody Talks About

Fintech users are not like other software users. They are managing money, often other people's money. A vague update note doesn't just confuse them; it triggers a risk assessment.

"Improved payment processing" could mean a performance optimization. It could also mean a change to how transactions are routed, which might affect settlement timing, which might affect their cash position, which might affect their own compliance obligations. They don't know which one it is. So they assume the worst and file a ticket.

The fix is not more words. It's more precision. Stripe handles this by maintaining a developer changelog that explicitly separates breaking changes from backward-compatible ones (Stripe, 2024). A breaking change is anything that could cause an existing integration to fail. A backward-compatible change is an addition that doesn't affect existing behavior. Global Payments uses the same taxonomy, labeling changes as [MAJOR] or [MINOR] in their API release notes (Global Payments, 2024). The labels do most of the work. A user who sees [MINOR] knows they don't need to test their integration. A user who sees [MAJOR] knows they do.

For non-technical users, the relevant question is not "what changed in the code" but "what changes for me." If a payment routing change doesn't affect settlement timing, say so explicitly. If it does, say that too, and say by how much. Finance teams don't need the technical implementation details. They need the operational impact.

The format that works in practice: a one-sentence summary of the change, a one-sentence description of who is affected and how, and a flag indicating whether action is required. That's it. The technical detail goes in the linked ticket for anyone who wants it.

Why the Workflow Breaks at Deployment Speed

Here is where the operational problem becomes acute.

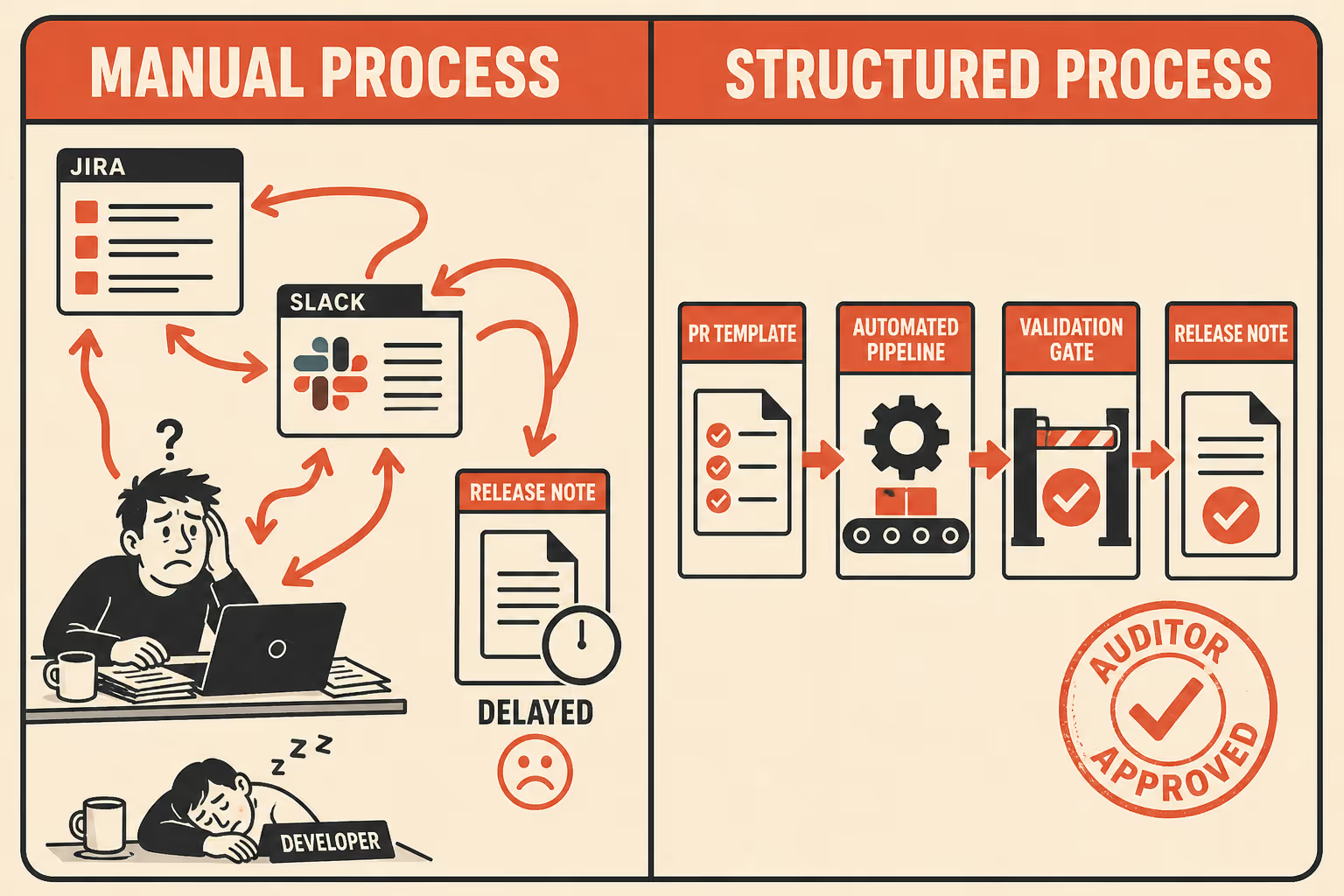

Most fintech engineering teams are deploying continuously, meaning multiple times per day, often across multiple services. The traditional release note workflow, where a technical writer or product manager manually compiles notes from Jira tickets and Slack threads at the end of a sprint, doesn't survive contact with continuous deployment (CD). Either the notes lag behind the deployments, which creates a gap in the audit trail, or they're rushed and vague, which creates the user trust problem described above.

Mews, a hospitality tech company, ran into exactly this problem when they moved to continuous deployment. With a few deployments per week, it was manageable for technical writers to monitor deployments and manually publish release notes. With deployment-per-closed-issue, it became impossible (Mews, 2019). Their solution was to treat release notes as a data entity in their system, automatically publishing them when a deployment was detected, with technical writers preparing the user-facing copy in advance and the system linking it to the deployment record.

The underlying insight is that the bottleneck is not the writing. It's the data collection. Manually extracting the relevant information from commits, tickets, and Slack threads at deployment time is slow and error-prone. The teams that have solved this problem are the ones that capture the intent and impact of a change at the moment it is written, not after it is deployed. Structured commit messages, pull request templates with required fields, and automated pipelines that extract this data from version control are the tools that make this possible (Ascend.io, 2025).

Research on automated release note generation confirms that the quality of the output depends almost entirely on the quality of the input. A 2025 study on LLM-powered release note generation found that models trained on well-structured commit messages and issue descriptions produce significantly more accurate and useful release notes than those working from unstructured commit histories (arXiv, 2025). The implication for fintech teams is that commit message hygiene and pull request discipline are not just engineering best practices. They are the upstream inputs that determine whether your release notes are compliant and useful or vague and risky.

The minimum viable process looks like this: a pull request template that requires a change type (breaking/non-breaking), a one-sentence user impact description, and a ticket reference. An automated pipeline that extracts this data from merged PRs and generates a structured draft. A final review gate where a product manager or technical writer validates the user-facing language and confirms the compliance fields are complete. The review takes minutes, not hours, because the draft already exists.

That's the model. Fast enough for continuous deployment. Precise enough for an auditor. Clear enough for a risk-averse finance team.

Doc Holiday generates structured release notes directly from version control and issue tracking, then provides a validation framework for compliance and user-facing review. The draft arrives from the engineering workflow; a technical writer or product manager runs final QA rather than drafting from scratch.